Medica Sur ($MEDICA)

A shareholder-aligned Mexican hospital at a discount to fair value

Quick Pitch

Ticker: MEDICA

Share Price: $41.00 MXN

Market Cap: $236m USD

EV: $264m USD

USD/MXN Rate: 17.30Medica Sur is a single-hospital operator in Mexico trading at 7.5x earnings while growing top line at 10% YoY

The company over-earned during the COVID era but management capitalized by selling its laboratory business and reinvested in core hospital operations

The market is discounting lower growth without the labs business but the remaining hospital operation has a long and durable growth runway ahead

Conservative balance sheet and owned real estate provide a large margin of safety

0.6x Net Debt/EBITDA

Real estate holdings conservatively valued at $125-165 million (>50% of the market cap)

Laser-focused on returning capital to shareholders via a combination of large dividends and aggressive buybacks

The company is locally listed. It does not have an ADR

Note: Medica Sur earns all revenue in MXN. For simplicity, I have converted historical figures to USD using yearly average FX rates.

Background

Medica Sur is a specialized private medical center in Mexico City located in the southern Tlalpan district (within walking distance of Estadio Azteca). The hospital operates 20 surgical units and 190 beds. Newsweek magazine has voted Medica Sur as the best Mexican hospital for the last 3 consecutive years. The hospital is also part of the Mayo Clinic Care Network, a group of 45 international healthcare organizations that get special access to the Mayo Clinic’s educational and research expertise. Medica was the Mayo Clinic’s first international partner and only affiliate in Mexico.

The company navigated the pandemic successfully and is set on a path of continued core revenue growth and shareholder returns. The company sold its laboratory businesses in 2021/2022 which resulted in a large cash windfall. Medica used proceeds for medical equipment investments, large dividends to shareholders, and buybacks. A quick summary of these events is important to contextualize share price action and management’s capital allocation strategy.

November 2021 → Sold its major lab division Laboratorio Medica Sur (LMS), which included Laboratorio Medico Polanco (LMP), to Synlab Group for a base price of $110 million

Medica received additional earnout and royalty payments of $5 and $26 million in 2021 and 2022, respectively

LMS and LMP operated 102 locations across multiple states in central Mexico and recorded $60 million in net sales for 2020

Medica Sur had purchased LMP in 2016, netting a nice gain on the sale

April 2022 → Sold the remainder of its lab business via the sale of Corporación de Atención Medica (CAM) to Synlab Group for $12 million

$10 million paid upfront, with a $2 million earnout payable in 2 years

CAM had 20 lab locations and recorded net sales of $2, $5, and $1 million in 2020, 2021, and 2022, respectively

August 2022 → Approved a special $26.83 peso/sh dividend, equal to $144 million, paid in September 2022

April 2023 → Approved another special $6.53 peso/sh dividend, equal to $39 million, paid in June 2023

Two other smaller dividends were paid during this period

May 2021 ($1.50 peso/sh) and May 2022 ($2.21 peso/sh)

Medica has repurchased 20% of its outstanding shares since selling its labs. The company has 99 million FDSO, down from 123 million in 2021

The company reports 108 million s/o but 9 million are held as treasury stock, subject to cancellation at the next shareholder meeting

Operating Results

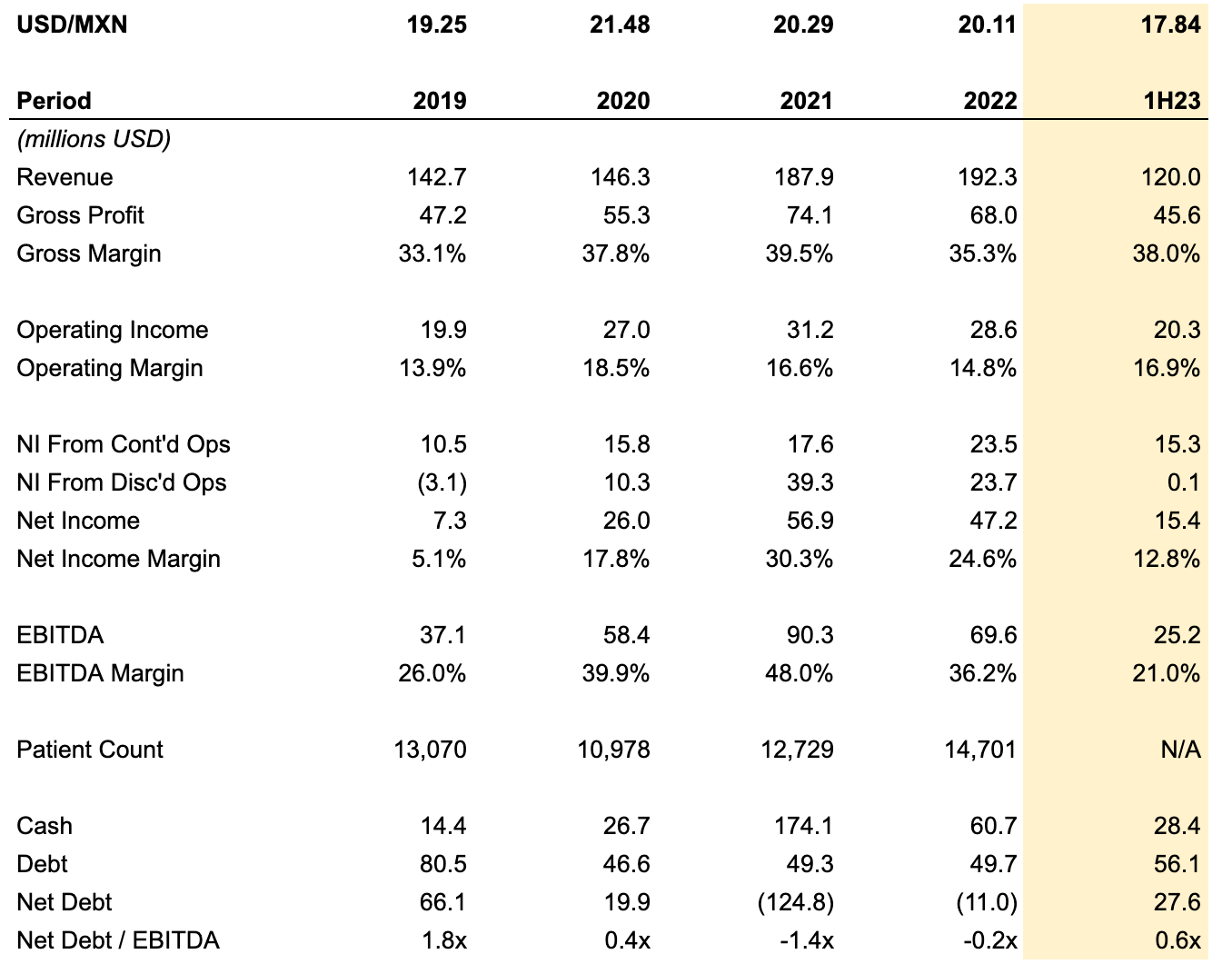

Operations over the past 4 years have not been straightforward given a large bump in lab testing revenue in 2020-2021 brought on by Covid-19, followed by the sale of the laboratory subsidiaries to Synlab Group in 2021 and 2022 in which the company recorded large gains on asset sales. I view these sales as well-timed and were likely done at peak or near peak earnings.

Medica amended its financials going back to 2019 to exclude discontinued operations from total revenue, but accounts for these effects in net income and EBITDA. This is useful for understanding normalized earnings for core hospital sales which have rebounded after most non-essential procedures were delayed during the pandemic.

Core hospital revenue continued to improve through 2022 but the bottom line was lower due to different sales mix and gains on asset sales, which were primarily recorded in 2021 with some spillover into 2022 (second lab sale transaction plus earnouts). Total patients treated in 2022 were 12% higher than the pre-covid base set in 2019.

Core hospital revenue for 1H23 increased 9.7% YoY while operating margin remained unchanged at 17%. The majority of discontinued operations and non-recurring items have been accounted for, painting a clearer earnings picture going forward.

Annualized capex for the business has hovered in the $7-10 million range for the past 4 years with the company generating $106 million in FCF from 2019-2022. Recent major capex investments include a $5 million investment in ERP software implementation (project "Núcleo”) expected to streamline operations, as well as the purchase of a state of the art MRI machine (GE 3.0 Signa Architect), the first model of its kind shipped to Mexico.

One final thing to note is that the company’s only debt is $58 million equivalent of 6.99% notes due in 2025 (denominated in MXN). Despite having $28m in net debt, the company has negative financing costs. This is because the current Mexican fed funds rate has risen to 11.25% which yields a nice return on the company’s cash balance.

Valuation

The company trades at at trailing 5.2x EBITDA multiple and 8.2x PE. At the current run rate, the multiples for FY23 look even cheaper at 5.0x EBITDA and 7.5x PE, respectively. The EBITDA multiple drops to less than 3x if you deduct $125m worth of real estate from the enterprise value (taking the lower end of RE fair value).

Medica has traded in a 5-9x EBITDA range going back to 2019 but is arguably in a much better financial position today, both in terms of profitability and balance sheet strength. The stock was valued at 22x earnings pre-covid and before selling the lab divisions.

The stock has traded in a tight range for the past year, mainly acting as a proxy for future dividend payments, but overall shareholder returns have been great factoring in these special dividends. As with many BMV listed names Medica shares have thin liquidity ($30k worth of shares traded per day) but I expect the stock can slowly rerate as the market realizes that core hospital operations continue to grow.

I think a high single digit or low double digit PE multiple can be justified by current financials. A 12x earnings multiple would imply ~60% upside without factoring further dividends or share repurchases.

The main drag to multiple expansion is that the company operates a single hospital and is naturally capped by occupancy and utilization, but I believe that Medica has significant growth runway ahead via pricing power and an uncontested leadership position in specialized care. In this context, selling its more commoditized lab business to reinvest in core hospital operations makes a lot of sense.

I expect the company to have material pricing power especially as Mexican income levels continue to rise and a more formal economy brings added medical insurance coverage. The company also boasts a medical tourism program citing its multiple awards and connections to the Mayo Clinic.

Final Thoughts

Neuco SA de CV is a majority holder, owning 50% of outstanding shares

In 2017 ProActive Capital, a private equity fund led by Jose Antonio Fernandez Carbajal, long-time CEO of Grupo FEMSA, announced a 40% purchase of Neuco, thereby controlling 20% of Medica Sur shares

Fernandez also sits on boards for universities such as MIT and Tec de Monterrey. I view his involvement here as a net positive

Overall there is limited information available on Neuco beyond ProActive’s ownership stake

Medica Sur has demonstrated shrewd management by buying and selling the labs business for material profit, successfully navigating the pandemic, and returning > $37 pesos/sh over the past 2 years in dividends alone

The real estate value is significant at $125-165 million and the company has taken an opportunistic approach to monetizing these assets at certain times

Sold its corporate offices in 2020 for $4 million (Calzada México-Xochimilco)

Entered into an agreement to sell 24,000 m2 of owned land (adjacent to Its hospital) to Grupo Sordo Madaleno in 2019 for $23 million, but the deal fell through due to a disagreement with local government

Mexico has said it will invest ~$6.6 billion for hosting the World Cup in 2026. Without a doubt many of these capital investments will go to estadio Azteca and its surroundings (which are within 1km of Medica Sur)

I do not expect Medica to sell + leaseback its main hospital real estate any time soon, but the company has multiple RE investment properties that it could continue to monetize

Medical insurance penetration remains low in Mexico with only 12 million people having coverage ~10% of the population

Insurance coverage rose 60% over the past decade

Additional growth in insurance coverage would be a positive revenue driver

According to Mexico’s INEGI (national polling service) only 3% of Mexican hospitals operate more than 50 beds, making Medica Sur one of the largest hospitals in the country and a leader in highly specialized care

nice writeup. mexico has all these interesting companies trading cheap. two questions if you know

1) Are they planning to set up any additional hospitals?

2) is most of their traffic domestic or via medical tourism (ie people coming from the US)

Will link to in my Monday EM link collection post... For more Mexican stock ideas:

Mexico Closed End Fund Stock Picks (Early 2023)

Mexico stock picks or potential nearshoring stocks that are the holdings of Mexico closed-end funds Herzfeld Caribbean Basin Fund, Mexico Equity and Income Fund, and The Mexico Fund.

https://emergingmarketskeptic.substack.com/p/mexico-closed-end-fund-stock-picks-early-2023